{kind=link}

Public debt ratios in Latin America and the Caribbean (LAC) increased by about 10 percentage points of GDP in 2020. With debt service costs rising, countries in the region are under pressure to cut public spending and/or raise taxes, even in the face of widespread needs to respond to the pandemic.

Our latest Regional Economic Outlook shows that well-crafted tax reforms can support growth while helping countries maintain fiscal sustainability. Importantly, these reforms can help reduce income inequality-an important objective in one of the most unequal regions in the world.

Tax structures in Latin America

Most LAC countries have a large tax collection gap relative to their potential, which can be explained only partially by the region’s level of development. LAC countries raise 13 percentage points of GDP less in tax revenue than the average OECD country, a gap that remains even after controlling for GDP per capita levels-which partly corrects for differences in informality, tax design and enforcement capacity. Since several LAC countries are, or are likely to become OECD members, OECD country averages are a natural benchmark.

There are also important differences in how LAC countries tax.

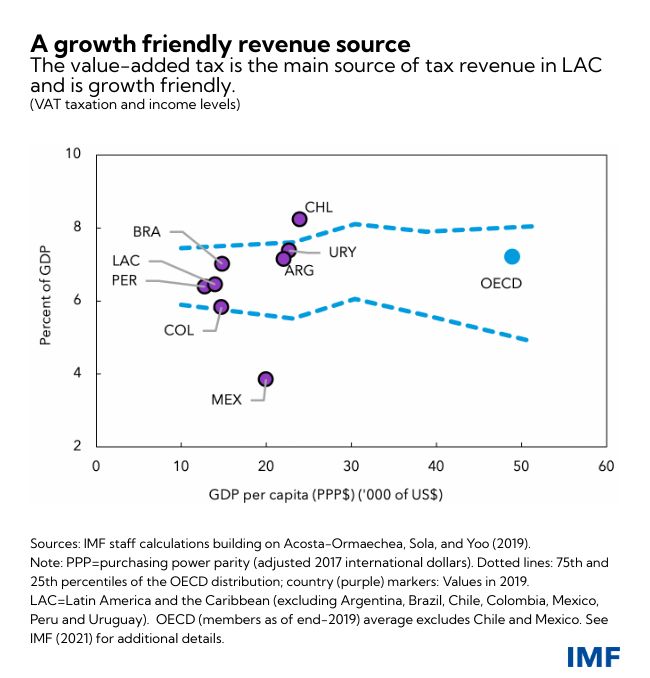

The main tax revenue source in LAC is the value-added tax (VAT). Its collection tends to be broadly aligned with the region’s level of development and is comparable to that of OECD countries (except for Mexico), but there is still room for improvement.

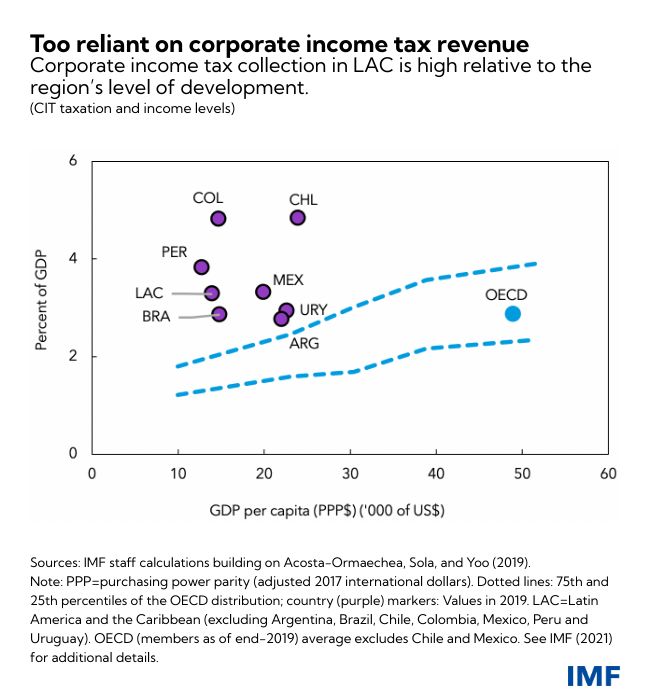

The share of corporate income tax (CIT) revenues in the region, however, is higher than in OECD countries and above what income levels would predict. Relying largely on corporate taxes negatively affects growth by discouraging investment.

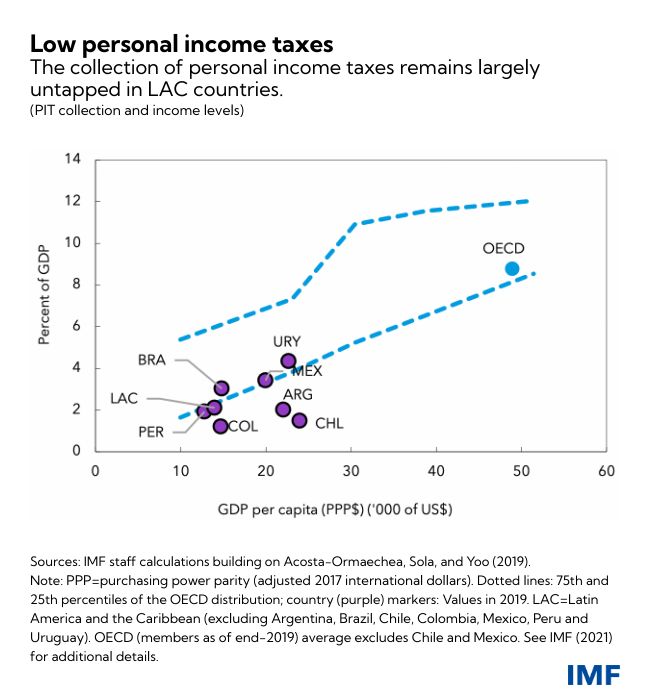

Conversely, the share of personal income tax (PIT) revenues in the region is low (but with promising results from reforms in Mexico and Uruguay that other countries could follow). When designed right, raising revenue through the PIT has a similar impact on growth as with the VAT (as seen in the OECD) and could help improve equity. More use of personal income taxes, combined with credits to incentivize labor force participation, and possibly fewer corporate taxes, could boost growth.

A better way to tax

Our analysis points to specific reforms that could help LAC countries tackle their fiscal, growth, and equity challenges.

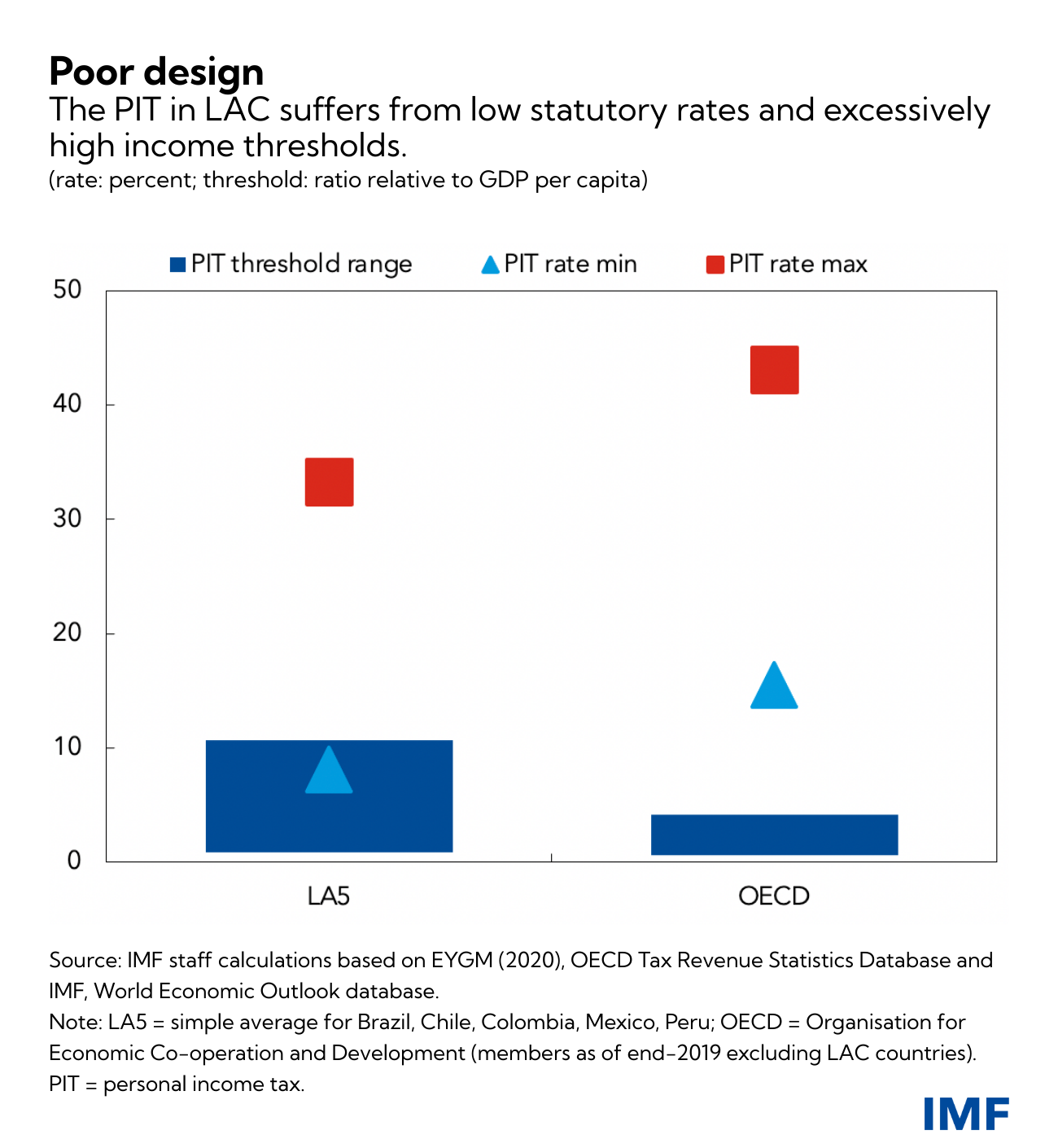

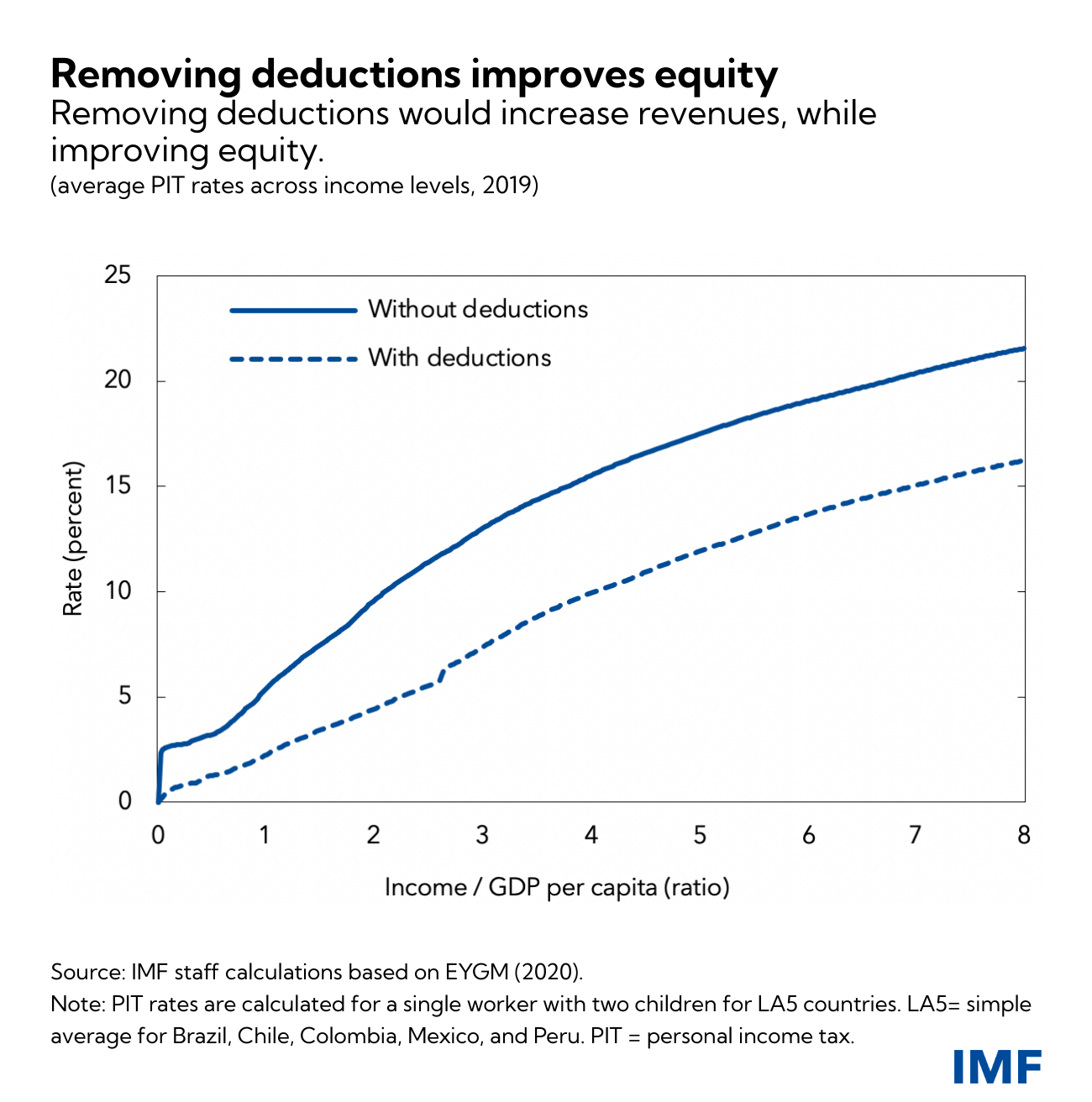

On the PIT front, there are clear design flaws in the region-low statutory rates, excessively high income thresholds, and widespread and regressive deductions (which tend to benefit the rich). These erode the tax base and worsen income distribution.

A worker in one of the five largest LAC economies (LA5)-Brazil, Chile, Colombia, Mexico and Peru– would have to earn 10 times the country’s GDP per capita to pay the maximum statutory rate for personal income taxes.

By comparison, that same worker living in an OECD country needs to earn an income of just 3.5 times the country’s GDP per capita to face the maximum PIT rate, which is on average significantly higher than that of LAC countries.

Reducing PIT deductions in LA5 countries would simplify the system, increase revenue, and make taxation more progressive-so an individual who earns more also pays more taxes-without levying additional taxes on low- or middle-income formal workers.

Leaving other parameters unchanged, if personal income tax deductions were eliminated (stripping the PIT system down to its statutory rates), the average LA5 country would see a twofold increase in PIT revenues, by raising the effective rate faced by the top 10 percent of wage earners. Importantly, this would also increase equity, since deductions disproportionally benefit rich households in LAC.

Providing well-targeted incentives to low-wage earners, through for example an earned-income tax credit (EITC), could encourage their participation in the labor market and help reduce the gender gap. It could also incentivize labor formalization by partially compensating social security contributions, helping improve revenue collection.

Reforms to the CIT could also be implemented. Aligning rates could help attract investment and alleviate profit shifting, while reducing tax benefits and deductions could level the playing field. Ongoing global corporate income tax reforms provide an important opportunity to revisit corporate taxation in LAC.

To address equity concerns, LAC countries could strengthen the VAT by tackling reduced rates and exemptions combined with well-targeted transfers that encourage the use of electronic payment methods (e.g. the social card program in Uruguay). The digital economy-further expanded due to the pandemic-should be taxed with the VAT the same way as other sectors in the economy to avoid tax base erosion.

Public support and timing are key

Public support is essential when implementing tax reforms. In a region where the perception and confidence that taxes are well spent is low, tax reforms would need to be accompanied with improvements in the quality and composition of public expenditure and in the overall fairness of fiscal policy.

Timing is also key. Until the pandemic is brought under control, it is important to continue supporting livelihoods to secure a robust recovery. Countries with tighter fiscal space may need to reform their tax systems earlier, which may help boost confidence in their medium-term fiscal frameworks.

***

Santiago Acosta Ormaechea is a Senior Economist in the IMF Western Hemisphere Department

Samuel Pienknagura Loor is an Economist in the IMF Western Hemisphere Department